High level presentation of P&L, Balance Sheet and operation metrics (Churn rate, LTV, CAC etc.)

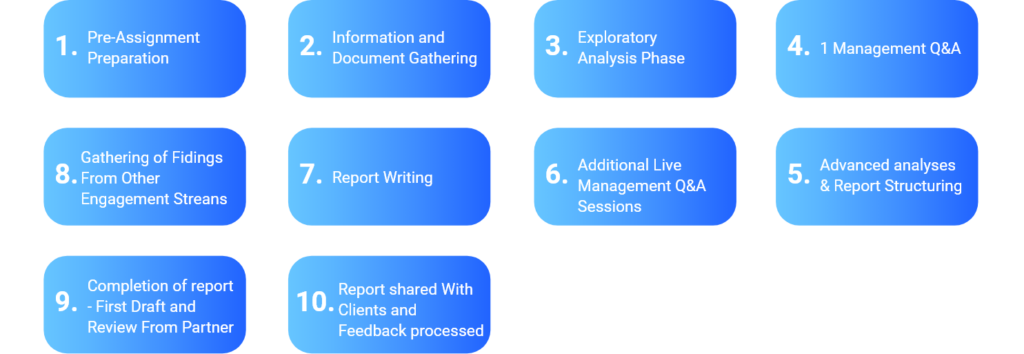

Review of target main sources of financial information

Descriptions of the different points of attention we recommend you to dig further and sort out with seller

List of items with the potential to be quality of earning adjustments and may impact the value of the deal

Detailed review of P&L, balance sheet and cash flow

Quality of earnings

In depth review of historical revenue and profit trends

Quality of net debt

Normalized net working capital analysis

Budget accuracy and assessment of forecast

Review of accounting principles used and their impact on financials

Direct call sessions with target’s Management

Reconciliation of different sources of information provided

Review of accounting principles used and their impact on financials

Check of cash position vs. bank statements

Get a comprehensive report on the financial health of the SaaS company under review

Understand historical business value drivers and shortfalls

Get an accurate picture of the SaaS business and operation metrics before investing

Deleverage your risk by identifying potential issues upfront

Get an assessment of the achievability of the team’s forecast

Base your SaaS valuation on adjusted and more reliable numbers

Spot any recent change in the SaaS business historical and recent trend that can impact the transaction

Use our quality of earnings, net debt, cash flow and net working capital adjustments as part of your negotiation with buyer

Gross and net churn rate, or customer retention figure

Lifetime customer value (LTV)

CAC/LTV

CAC payback period

Customer acquisition cost (CAC), also called customer lifetime value

How are returning customers, upgrades and downgrades taken into account in the customer churn calculation?

Is the LTV a basic customer lifetime value calculated as 1/customer churn rate or is this metric based on more accurate historical numbers.

What costs are allocated to the CAC ? And are these allocated costs properly allocated by product?

Are the metrics monitored on a simple basis or on a cohort basis?